Divorce is never simple—but when one spouse serves in the military, the process becomes even more complex. From federal protections to unique benefits like pensions and healthcare, a military divorce involves rules and considerations that don’t apply in civilian cases. If you or your spouse is in the armed forces, understanding these differences can help you make smarter decisions and avoid costly mistakes.

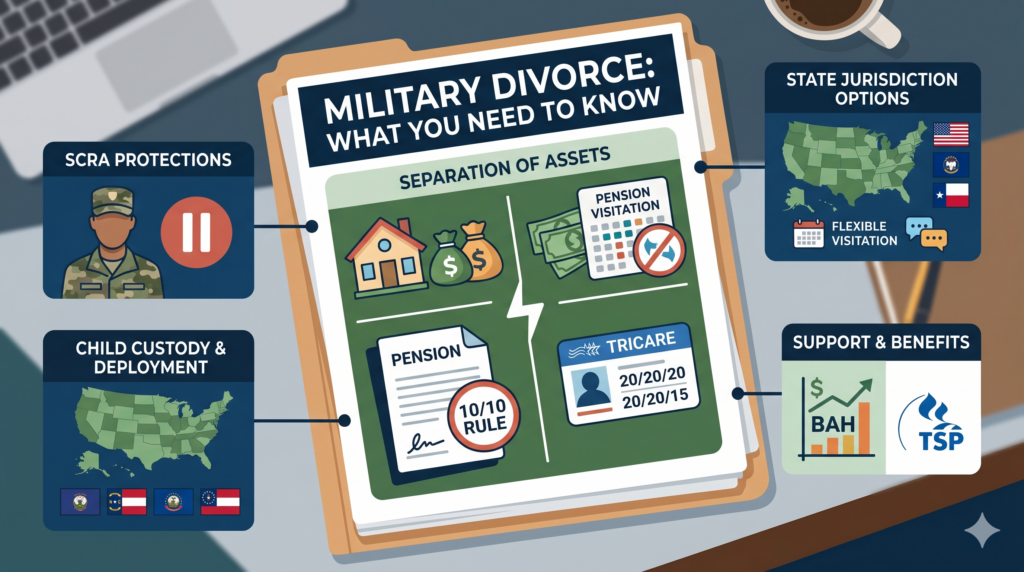

Understanding Where to File

One of the first and most important decisions in a military divorce is where to file. Unlike civilian divorces, you may have multiple options:

- The state where the service member is stationed

- The state of legal residence

- The state where the non-military spouse lives

Each state has its own laws governing property division, alimony, and child support. Choosing the right jurisdiction can significantly affect the outcome of your case, so it’s worth careful consideration.

Protections for Active-Duty Service Members

The Servicemembers Civil Relief Act (SCRA) is a federal law designed to protect active-duty military personnel from being disadvantaged in legal proceedings due to their service. It allows service members to request a temporary delay in divorce proceedings if their duties prevent them from participating.

This doesn’t stop the divorce entirely—it simply ensures that the service member has a fair opportunity to respond and be present.

Dividing Military Retirement Benefits

Military pensions are often one of the most valuable assets in a marriage. Under the Uniformed Services Former Spouses’ Protection Act (USFSPA), state courts can treat military retirement pay as marital property and divide it accordingly.

A key concept to understand is the 10/10 rule:

- 10 years of marriage

- 10 years of overlapping military service

If this rule is met, the former spouse can receive payments directly from the Defense Finance and Accounting Service (DFAS). If not, the court can still award a portion of the retirement—it just won’t be paid directly.

What Happens to Military Healthcare?

Healthcare is another major concern. Through TRICARE, military spouses may be eligible for continued coverage after divorce—but only under specific conditions.

- 20/20/20 Rule: Full benefits continue if the marriage, service, and overlap each lasted at least 20 years

- 20/20/15 Rule: Provides limited, temporary coverage (usually up to one year)

If you don’t meet these thresholds, you’ll need to explore alternative health insurance options.

Housing and Financial Support

Military compensation includes housing allowances (BAH), which can complicate financial arrangements during separation. While still married, the military may require the service member to provide financial support to their spouse.

After the divorce is finalized, those benefits typically end unless there are dependent children involved.

Child Custody and Deployment Challenges

Child custody in military families often requires extra planning. Frequent relocations, deployments, and irregular schedules can make traditional custody arrangements difficult.

Courts prioritize the best interests of the child, but parenting plans often include:

- Flexible visitation schedules

- Provisions for temporary custody during deployment

- Communication plans for long-distance parenting

Spousal and Child Support

Spousal support (alimony) is determined by state law, but military income—including base pay and allowances—is typically factored into calculations. Temporary support may also be required while the divorce is pending.

Child support is also governed by state guidelines, though military pay structures can influence the final amount.

Don’t Overlook Other Military Benefits

Beyond retirement and healthcare, there are additional benefits that may come into play:

- Survivor Benefit Plan (SBP)

- Thrift Savings Plan (TSP)

- Commissary and exchange privileges (in limited cases)

These benefits must be specifically addressed in the divorce agreement. Missing or vague language can result in lost entitlements.